The pandemic did not invent any new loyalty behaviors. What it did was compress a decade of slow-moving change into roughly nine months — and in doing so, it exposed which loyalty programs were genuinely valued by their members and which were quietly tolerated. For operators, the period from early 2020 through late autumn offered a once-in-a-generation natural experiment: every assumption about how customers behave inside a rewards program was tested under conditions no playbook had prepared for.

This piece synthesizes what the research community has learned about loyalty behavior during the disruption, and what it tells us about the structural choices that made some programs resilient while others bled members quietly.

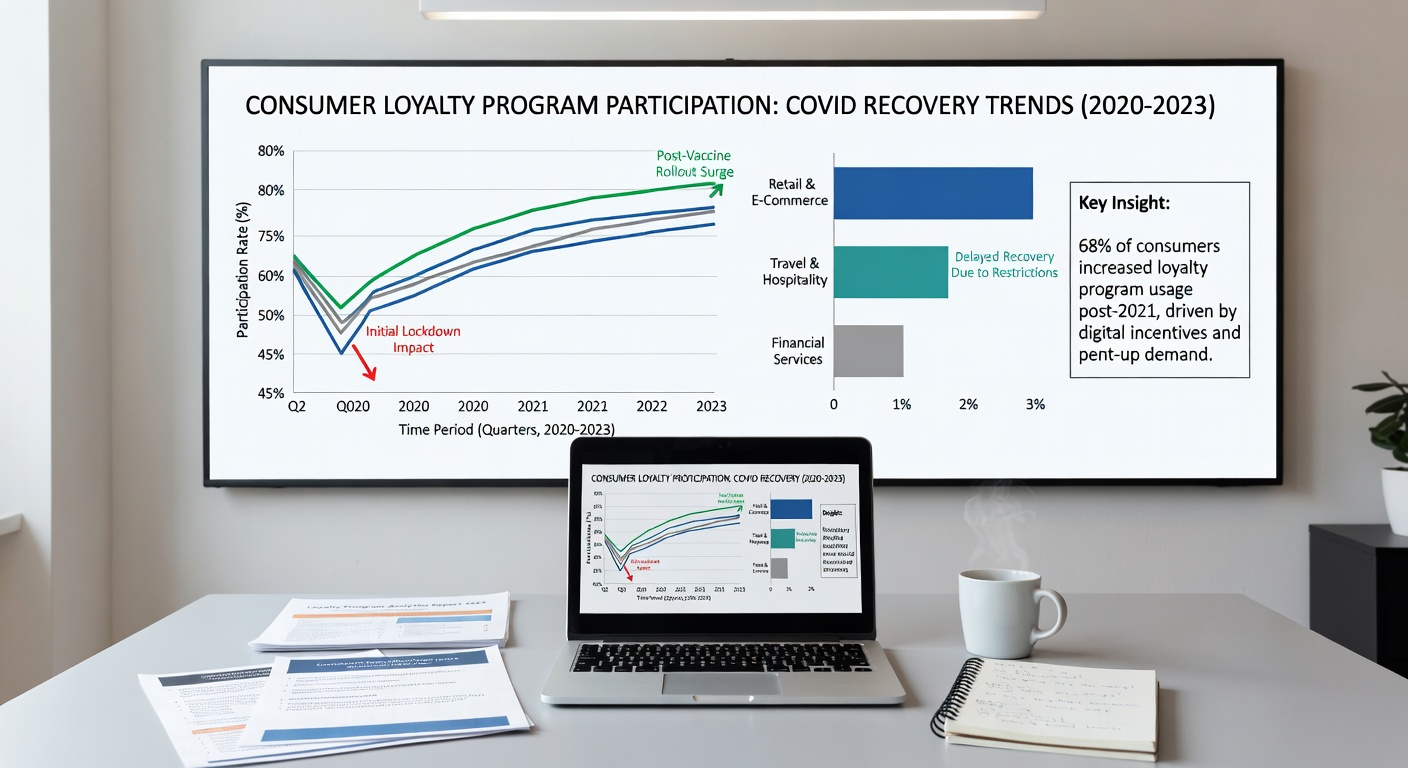

The Enrollment Shift Was Not Uniform

Aggregate loyalty enrollment numbers from 2020 are misleading because they smooth over enormous category-by-category swings. Grocery, quick-service restaurant, and pharmacy programs saw enrollment spikes as consumers consolidated trips and looked for ways to stretch household budgets. Airline, hotel, and dining loyalty programs experienced the opposite: a near-freeze in new sign-ups and a sharp drop in active engagement among existing members who simply had nowhere to use their status.

The pattern that emerged was not “loyalty is up” or “loyalty is down.” It was a category reshuffling, with consumers reallocating their loyalty attention toward the brands they were actually still transacting with. Programs that required physical presence to earn or redeem fell out of weekly habit. Programs that could be used from home — or for essentials customers were going to buy anyway — moved up the priority list.

Hoarding, Then Burning

One of the most studied behavioral patterns during the disruption was the shift in redemption behavior. Early in the year, redemption rates dropped across most categories. Members held on to points and miles, partly because there was nothing worth redeeming for, and partly because of a defensive instinct around accumulated value.

By the second half of the year, the pattern reversed in some categories. As programs extended status, expanded redemption options into everyday categories like groceries and streaming, and added flexibility, members who had been sitting on points began to burn them — sometimes aggressively. This was particularly visible in travel programs that pivoted to letting members redeem miles for merchandise, gift cards, or charitable donations.

The lesson for operators was structural: programs with rigid redemption catalogs lost engagement. Programs that quickly broadened “what your points can do” preserved it.

The Digital Adoption Curve Snapped Forward

If there is one undisputed story from the period, it is the acceleration of digital loyalty. Contactless redemption, in-app earning, mobile wallet integration, and digital-only program launches saw adoption levels that internal roadmaps had penciled in for 2023 or later. Customers who had never downloaded a brand app downloaded one in a week. Customers who had never used a QR code to identify themselves at checkout used one daily.

This was not a temporary spike. The behavior stuck. Once members became comfortable with digital identification, mobile reward redemption, and app-based offers, very few rolled back to physical cards. Programs that had been investing in digital infrastructure ahead of the disruption found themselves with a usable advantage. Programs still running on plastic cards and printed coupons faced a forced modernization without the budget cycle to plan it properly.

“Stood By Their Customers” Became a Loyalty Signal

Research on consumer sentiment during the year showed a recurring theme: members noticed which brands extended status, paused points expiration, and communicated transparently about program changes — and which brands quietly tightened terms when members were least able to push back.

This is more than a customer service observation. It is a loyalty design lesson. Programs are contracts, and the disruption put the soft terms of those contracts under a microscope. Members who felt their brand “stood by them” reported higher likelihood to remain active post-recovery. Members who felt the brand had taken advantage of the disruption reported lower trust — and that lower trust translated into reduced wallet share over the following quarters.

Flexible Programs Outperformed Rigid Ones

Across categories, the structural finding was consistent: programs designed with flexibility — multiple ways to earn, multiple ways to redeem, low friction to switch between rewards — held member engagement better than programs designed around a single linear earn-and-burn flow.

A frequent-flyer program with only flight redemptions lost engagement faster than one that allowed miles toward merchandise, hotels, or partner brands. A coffee program with only “free drink” rewards lost engagement faster than one that let members redeem toward merchandise or pay-it-forward charitable options. The principle is straightforward: when one part of the customer’s life is disrupted, the program needs to still be useful for the parts that aren’t.

What the Disruption Revealed About Loyalty Psychology

Looking across the research, three structural truths about loyalty psychology became visible:

First, accumulated value is emotionally heavier than expected. Members do not treat points as throwaway currency. They treat them as savings, and reactions to expiration or devaluation are disproportionate to the dollar amount involved.

Second, loyalty is contextual. The same member can be deeply loyal to a brand in one life-mode (commuting to an office) and indifferent to it in another (working from home). Programs designed for one context fall out of habit fast when the context changes.

Third, communication is part of the program. The frequency, tone, and transparency of program communications during the disruption affected retention almost as much as the program economics did. Programs that disappeared from member inboxes were forgotten. Programs that communicated thoughtfully — without pestering — held their place.

FAQ

Did the disruption permanently change loyalty program design? The disruption accelerated changes that were already underway: more digital, more flexible redemption, more emphasis on emotional engagement. It did not invent new design principles so much as raise the cost of ignoring them.

Did members trade down to cheaper programs? In categories where consumers were under budget pressure, yes — some traded down from premium loyalty tiers to value-oriented programs. But the trade-down was not as universal as early commentary suggested.

Which industries recovered loyalty engagement fastest? Categories with continuous everyday utility — grocery, pharmacy, quick-service restaurant — recovered first because their members never stopped engaging. Travel and event-based programs recovered more slowly and unevenly.

Should operators design for “the next disruption”? Operators should design for flexibility as a default — multiple earn paths, multiple redemption options, communication infrastructure that can pivot quickly. The specific disruption is unpredictable; the need for adaptive program architecture is not.

The Underlying Lesson

The most useful framing that has emerged from the year is this: the disruption did not change what loyalty is. It changed what loyalty programs need to be in order to deliver on it. The brands that came through with their member relationships intact were the ones whose programs were already designed to flex — and whose communications, during the worst of it, sounded like a brand talking to a friend rather than a system sending a notification.

Further Reading from Authoritative Sources

- Harvard Business Review — HBR publishes the behavioral economics and consumer psychology research that underpins the article’s analysis of hoarding behavior, contextual loyalty, and the disproportionate emotional weight members assign to accumulated point balances.

- National Retail Federation — NRF published research on how restaurant and retail loyalty programs were affected by the pandemic disruption, providing the category-level enrollment and engagement data that contextualizes the COVID loyalty behavior analysis in this article.