There was a stretch in late 2011 and through 2012 when casual dining operators were unsure whether loyalty programs would actually work in their format. The QSR template that Starbucks had pioneered did not translate cleanly to a $20 check at a steakhouse, and several early casual dining launches had struggled to produce the visit lift their business cases assumed. By the first quarter of 2013, the picture had brightened enough that operators who had been on the sidelines started moving from skepticism to active planning. This piece looks at what changed in the early-2013 consumer data and why those signals were genuinely encouraging.

Consumer willingness was no longer the bottleneck

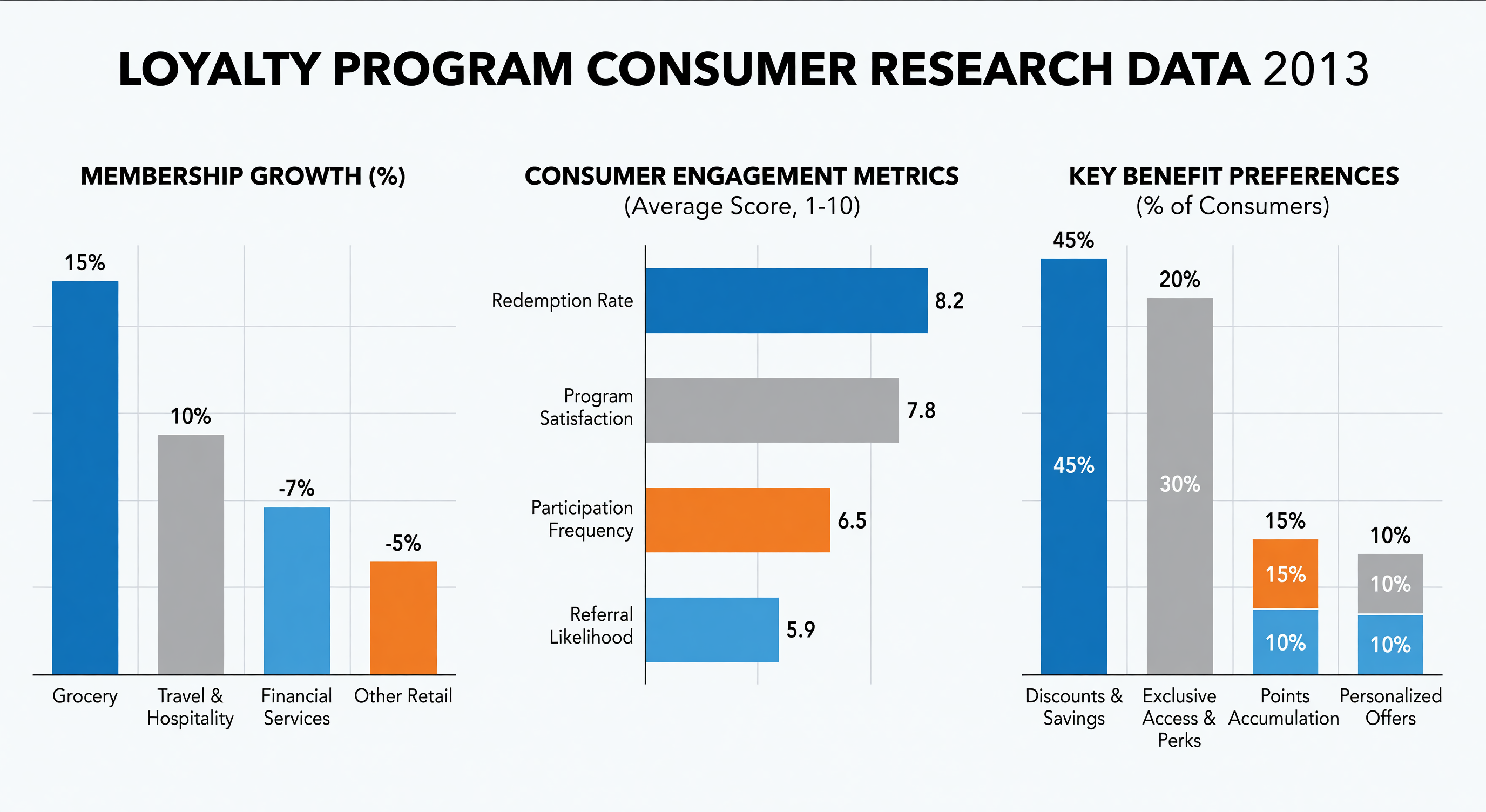

The first encouraging signal was that consumer interest in restaurant loyalty had crossed a threshold. By early 2013, a clear majority of casual dining customers said they were willing to enroll in a program at a brand they visited regularly, and a meaningful minority reported actively seeking out programs at brands they were considering. The behavioral resistance that had limited casual dining loyalty growth in 2011 had largely dissolved.

This mattered because it removed the most common excuse for not launching. Operators no longer had to argue against the worry that their guests “would not want another card.” The data said clearly that guests did want one, provided the rewards were tangible and the enrollment process was painless.

Redemption was finally producing real lift

The second encouraging signal was that 2013 casual dining redemption data was producing measurable check lift on visits where members redeemed. The pattern was consistent across formats: members who redeemed a reward visited again sooner, brought more party members on average, and added incremental items to the check beyond the redeemed item. The reward was not cannibalizing future spend — it was anchoring the next visit.

This finding addressed the second-most-common operator objection. The fear that “free entree rewards just give away food we would have sold anyway” turned out to be largely wrong for engaged members. The free entree reset the visit cycle and pulled the member back in faster than they would have returned otherwise.

Mobile created a viable casual dining engagement model

The third encouraging signal was the early evidence that mobile could carry casual dining loyalty engagement the same way it was carrying QSR loyalty. Casual dining brands had been slow to invest in apps in 2011 and 2012, in part because the visit frequency at a $25 dinner check did not seem to justify a dedicated app. By early 2013, the data was suggesting that members who downloaded a casual dining app behaved much more like QSR loyalty members — checking in more often, responding to push offers, and visiting at higher frequency.

For more on how operators began structuring program launches around these signals, see our loyalty program roadmap piece.

The 2013 outlook

The combined message from early 2013 was that the foundational consumer behaviors needed for casual dining loyalty to work were in place. Willingness to enroll was high. Redemption produced real lift. Mobile was beginning to scale. The remaining challenges were operational and strategic: choosing the right program structure, training staff to drive enrollment and redemption at the point of sale, and investing in the analytics needed to manage the program after launch. None of those challenges were small, but they were manageable in ways that consumer resistance would not have been.

FAQ

Why was 2013 considered a turning point for casual dining loyalty? Consumer willingness to enroll crossed a clear majority threshold, redemption began producing measurable check and visit lift, and mobile engagement started to scale in casual dining the way it had already scaled in QSR.

Did redemption rewards cannibalize future spend at casual dining brands? For engaged members, no. Redemptions reset the visit cycle and pulled members back sooner than they would have returned without the reward.

What was holding casual dining loyalty back before 2013? A combination of operator skepticism, weak early business case results, and uncertainty about whether the QSR loyalty playbook would translate to higher check averages.

Further Reading from Authoritative Sources

- National Retail Federation — NRF tracks consumer attitudes toward loyalty program participation across the restaurant industry, providing industry-wide context for the 2013 turning-point trends described in this article.

- loyalty program — Wikipedia provides a foundational overview of loyalty program history that contextualizes the casual dining adoption wave of 2012–2013.